September 7, 2021, updated October 6, 2023

—

Flooding can strike at any time, leaving a path of destruction and damage behind for people, communities, and states to contend with. Hurricane Ian’s impact on the U.S. Southeast last year exemplifies how quickly flooding can uproot communities: neighborhoods were inundated, over 150 lives were lost, and over $112 billion in damages were caused by Ian, the costliest hurricane in Florida’s history. Just a few weeks ago, record rainfall brought intense flooding to much of New York City, halting public transportation and transforming streets into rivers. In 2023 alone, there have been 23 confirmed weather disaster events, each with losses of more than $1 billion.

Flooding can be financially devastating to households – just one inch of rain can cause $25,000 of damages to an average home. And flooding threatens communities regardless of whether they sit near a coastline; in the last 25 years, 99% of U.S. counties have been damaged by a flooding event. As extreme rainfall and flash floods intensify and become more frequent, people must manage the risk that flooding poses to their property and take proactive measures to support a quick recovery in the event of a disaster.

That’s where flood insurance comes in. Flood insurance can help individuals, businesses, and communities prepare for and recover from disasters by protecting buildings and belongings when flooding strikes. As of April 2022, the Federal Emergency Management Agency (FEMA) implemented a significant change to the National Flood Insurance Program (NFIP) that further helps communities protect themselves while adapting to the reality of more frequent flooding.

The updated methodology that FEMA now uses for pricing flood insurance, called Risk Rating 2.0, ensures that flood insurance rates reflect an individual property’s risk and replacement value. Under these and other more precise criteria, Risk Rating 2.0 actually reduced premiums for many policyholders across the country.

If you are:

- A property owner or renter considering purchasing flood insurance;

- Someone concerned or seeking more information about Risk Rating 2.0; or,

- A community leader or property owner interested in taking steps to reduce the physical and financial risks posed by flooding;

Then take five quick minutes and read on. In this article, we will introduce the basics of flood insurance, Risk Rating 2.0, and other steps to reduce flood risk. Risk Rating 2.0 is modernizing NFIP by ensuring flood insurance rates are based upon each individual property’s risk to flooding and improves equity by reducing insurance premiums for policyholders who were previously paying more than their fair share for flood insurance.

Why flood insurance?

Before we dive into the ins and outs of Risk Rating 2.0, we’ll first cover the basics of flood insurance. Flood insurance covers buildings and belongings impacted by water damage specifically due to flooding.

Although FEMA manages the National Flood Insurance Program, people generally buy their NFIP policies through private insurance companies — the same companies that sell homeowners and car insurance. As most homeowners or renters insurance does not cover flood damage, homeowners with federally-guaranteed mortgages within flood zones must purchase flood insurance, in addition to homeowners or renters insurance.

How much does it cost?

Average costs for flood insurance vary by state — low of $430 per year in Maryland to a high of $1300 in Vermont. The average annual flood insurance premium is about $900. Annual flood insurance premiums may change from year to year, as part of a gradual process to make premium rates reflect accurate flood risk. Current law limits rate increases to no more than 18% per year. Known as a premium cap, this rate limit ensures that policyholders do not unexpectedly face a full raise in premium cost in a single year.

Who needs flood insurance?

The federal government requires that homes in high-risk flood areas backed by a federal mortgage are protected by flood insurance. To see whether a property lies in an area that triggers the mandatory purchase requirement, visit FEMA’s Flood Map Service Center or the First Street Foundation’s Flood Factor tool.

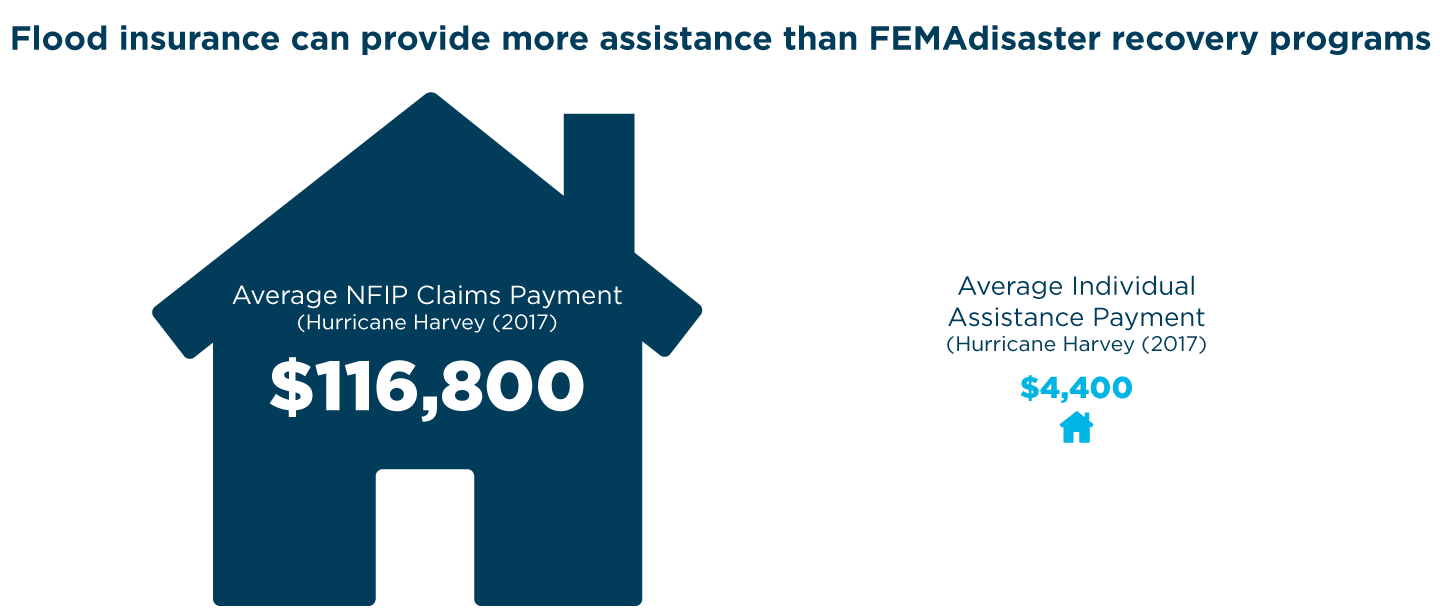

Flood insurance is also a good idea for homeowners living outside these zones: Between 2015 and 2019, more than 40% of NFIP flood claims came from properties outside the high-risk flood areas. Although programs like FEMA Individual Assistance (IA) can provide financial help and direct services to help after a presidential disaster declaration, average IA payments pale in comparison to the average NFIP claim. After Hurricane Harvey in 2017, the average NFIP claim was about $116,800 while the average IA payment was only $4,400. Purchasing a flood insurance policy is one of the best ways that individuals can protect themselves from the financial impacts of a flood disaster.

The bottom line: floods are financially devastating, and are capable of tearing apart properties and communities in a matter of hours. But with flood insurance, people have peace of mind that they will have necessary resources to recover if faced with a disaster.

What is Risk Rating 2.0?

Starting in 2021, FEMA began implementation of Risk Rating 2.0, which updated NFIP rates to focus more on an individual property’s risk. This was the first time in over 50 years that FEMA has significantly adjusted the methodology for pricing flood insurance premiums for NFIP.

What were the changes?

Previously, FEMA’s rating methodology was a “one-size-fits-all” approach that priced flood insurance based on which flood zone a property was mapped in by FEMA. Practically, this meant that two houses located right next to each other could have vastly different insurance premiums if they were mapped in different flood zones by FEMA.

Since implementation of Risk Rating 2.0, flood insurance rates are now decided at the individual property level in order to give policyholders a more accurate and transparent picture of flood risk for their home.

FEMA now considers new factors when calculating flood insurance rates, including the different types of flooding that could impact a property (including riverine and flash flooding), the distance a property is from a source of flooding like the coast or a river, and the cost to rebuild or restore that property. This creates unique insurance rates that accurately reflect an individual property’s risk. Because homeowners and renters are now paying for their property’s individualized risk and replacement value, the system is fairer.

Some elements of flood insurance did not change with Risk Rating 2.0. For example, the mandatory purchase requirement is still in place, along with the premium cap that limits rate increases to no more than 18% per year.

How does Risk Rating 2.0 affect flood insurance premiums?

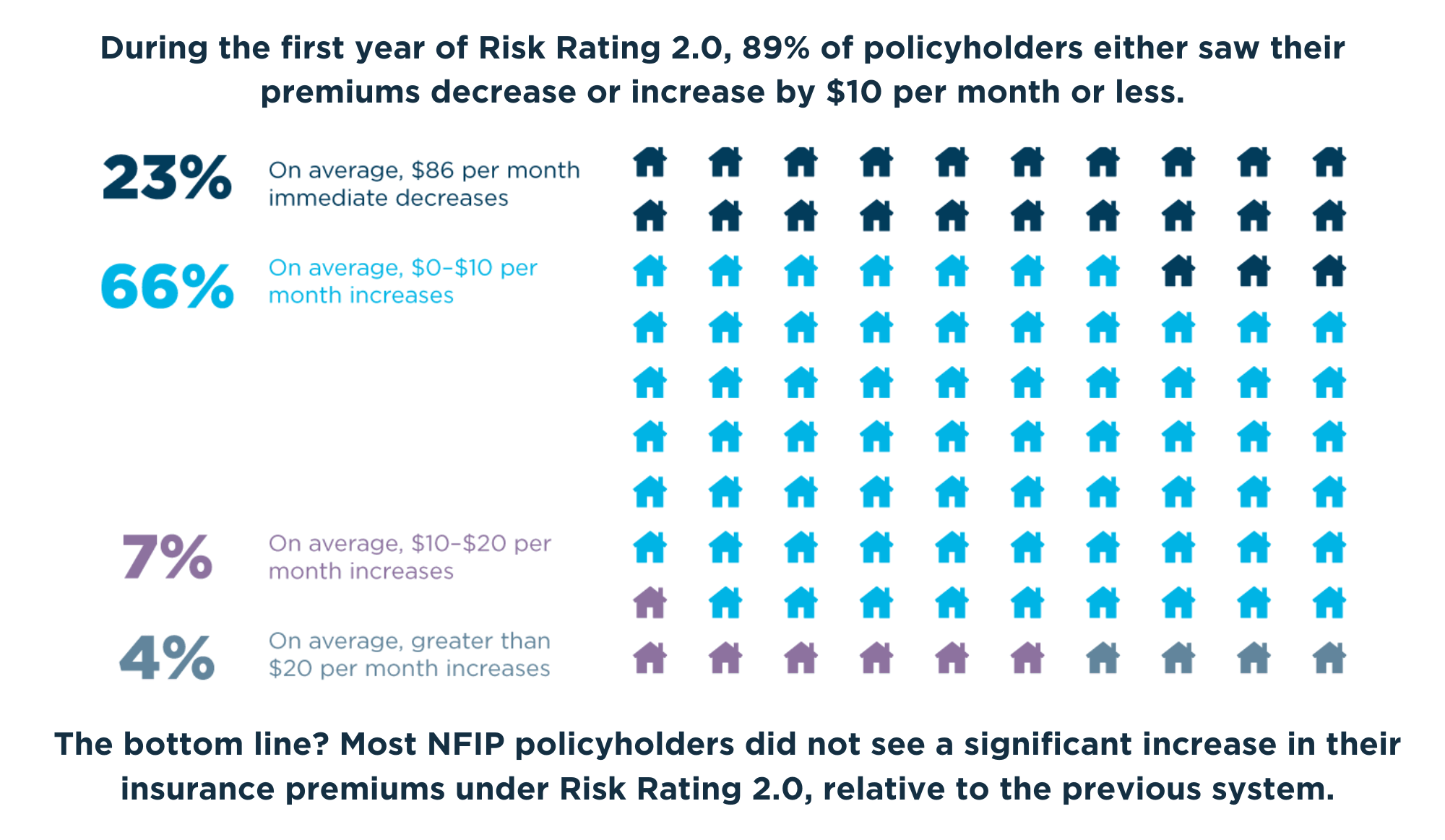

Under the previous system, policyholders on average saw premium increases of $8 per month. In the first year of Risk Rating 2.0, 89% of current policyholders saw their premiums either immediately drop or increase by no more than $10 per month, according to estimates by FEMA. In other words, most policyholders saw a lower rate under Risk Rating 2.0, or only a very small change in their monthly premium consistent with annual increases under the previous system.

Additionally, with each passing year since Risk Rating 2.0 took effect, more policyholders will reach their full risk-adjusted rate – the rate that FEMA has determined is the accurate rate for the property. Once policyholders are paying their full risk-adjusted rate, they should no longer see premium increases, barring any changes to a property or its overall risk. This is also an important change from the previous system where rates never decreased.

Under FEMA’s old pricing methodology, policyholders with lower-valued homes were paying more than their share of the risk while policyholders with higher-valued homes were paying less. This is because FEMA did not consider costs required to rebuild a home if necessary under its previous pricing calculation. Homes with higher values cost more to reconstruct, so Risk Rating 2.0 makes the system fairer by ensuring home values and premiums are aligned with a property’s actual risk.

Other ways to prepare for floods

Though incredibly important, buying flood insurance is only one way to prepare for floods. Communities can also invest in efforts that reduce flood risk. And these efforts can pay off with both reduced damage and reduced premiums.

Take individual mitigation efforts

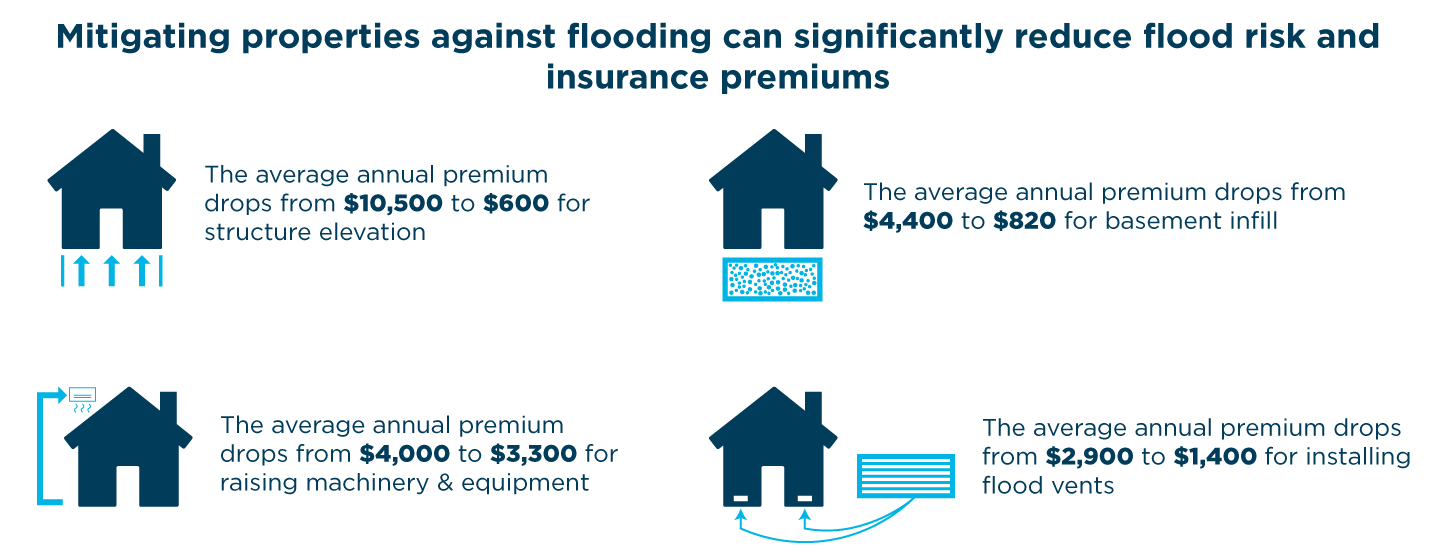

Because mitigation efforts to properties — such as elevating a building or installing proper flood openings in a crawlspace — help reduce flood damage, FEMA incentivizes such efforts with reduced premiums for NFIP policyholders. One study found that for elevating a structure in New York City, the average annual premium drops from $10,500 to $600; for basement infill, premiums can drop from $4,400 to $820.

Under Risk Rating 2.0, more policyholders are now receiving discounts for taking actions to reduce flood risk to their property (such as elevating a structure, installing flood openings, or elevating machinery and equipment) than under the previous system. Due to the expansion of mitigation discounts, six times more policyholders are now receiving credit for elevating insured properties, according to data from FEMA.

Enroll in the Community Rating System

To reduce the potential impact of flood insurance costs, local leaders can enroll their municipality in FEMA’s Community Rating System (CRS) program. Through direct reductions in federal flood insurance premiums, CRS gives local communities credit for taking steps to reduce flood risk. This program allows local leaders to deliver flood insurance cost reductions directly to most, if not all, residential flood insurance policyholders in their community.

Communities can earn National Flood Insurance Program rate discounts of 5–45%, based on the CRS classification. For more on CRS, read our blog post on how communities can protect property values.

Use American Flood Coalition resources

The American Flood Coalition created the Flood Funding Finder, an interactive website that uses a robust filtering system to prioritize the needs of small communities and help them identify the right federal funding programs to fund flood resilience.

The Flood Funding Finder features programs like FEMA’s Flood Mitigation Assistance program, which communities can use to support structure elevation projects to mitigate flooding and in turn potentially reduce flood insurance premiums.

AFC’s Adaptation for All guide can also help local leaders determine the approaches to flooding or sea level rise that can work best for them. Drawing on examples from the U.S. and the Netherlands — a country with a long history of flood challenges and innovations — this guide highlights 26 approaches that can help communities of any size determine the projects that best fit their flood resilience strategies.

Flood insurance is a cornerstone for building a culture of preparedness and resilience, especially when paired with complementary efforts to reduce vulnerability to flooding. Risk Rating 2.0 updated insurance pricing to more accurately reflect risk, creating a fairer system. While flood insurance does not physically protect property from floodwaters, purchasing a NFIP policy is the best way that individuals can prepare ahead of time to recover quickly after a flood disaster.